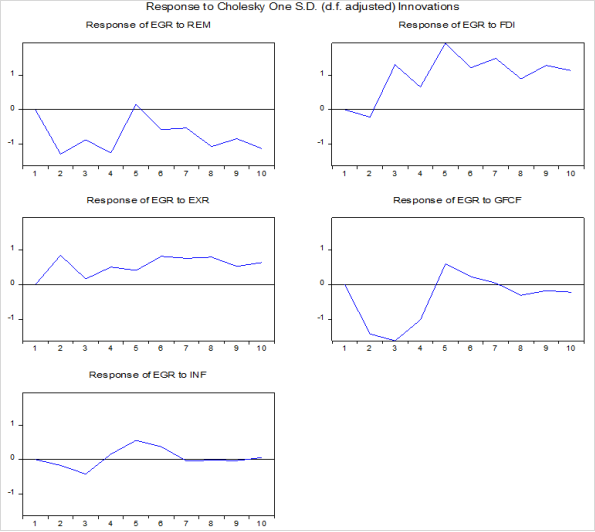

The globalization of the world economy, coupled with the recent rise of anti-globalization sentiments in some regions, has made it challenging for underdeveloped nations like Nigeria to fully understand the drivers of economic growth. After gaining independence, Nigeria, like many other growing economies in sub-Saharan Africa, has been striving to achieve and sustain long-term economic growth. The recent downturn in FDI can be attributed to recurring political instability, sluggish economic growth, and a weak global economy, leading to dwindling investment in manufacturing and related sectors. Consequently, examining the long-term relationship between remittances, FDI, and economic growth is crucial for policymakers and government advisers. The present study sought to appraise the relationship among remittance inflow, foreign direct investment (FDI), and economic growth in Nigeria. Time series data, which spanned the period of 1986-2022, was utilized. The vector error correction model was employed for the estimation. From the study, remittance was found to have a negative and non-significant relationship with economic growth. A bi-directional causation was established between FDI and economic growth. Lastly, remittance had no significant relationship with foreign direct investment. The study hence recommends that policymakers should draw up sufficient FDI inflow strategies that would translate to economic growth. This could be done through building confidence in the domestic economy through political stability and cooperation with relevant stakeholders.

| Published in | International Journal of Economic Behavior and Organization (Volume 13, Issue 2) |

| DOI | 10.11648/j.ijebo.20251302.12 |

| Page(s) | 74-85 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Foreign Direct Investment, Economic Growth, Investments, Remittances Inflows

EGR | REM | FDI | EXR | GFCF | INF | |

|---|---|---|---|---|---|---|

Mean | 4.162427 | 3.030160 | 1.582739 | 131.1854 | 30.74020 | 19.42647 |

Median | 4.195924 | 2.857986 | 1.380374 | 125.8081 | 28.64594 | 12.87658 |

Maximum | 15.3291 | 8.333830 | 5.790847 | 425.9792 | 54.94827 | 72.83550 |

Minimum | -2.03511 | 0.004883 | -0.03912 | 1.754523 | 14.16873 | 5.388008 |

Std. Dev. | 3.854065 | 2.430854 | 1.257269 | 118.7234 | 12.70218 | 17.32921 |

Skewness | 0.515553 | 0.271489 | 1.655711 | 0.910852 | 0.300443 | 1.764587 |

Kurtosis | 3.459191 | 1.857488 | 5.799086 | 3.034101 | 1.910055 | 4.837096 |

Jarque-Bera | 1.964139 | 2.466912 | 28.98395 | 5.117979 | 2.388109 | 24.40456 |

Probability | 0.374535 | 0.291284 | 0.000001 | 0.077383 | 0.302990 | 0.000005 |

EGR | REM | FDI | EXR | GFCF | INF | |

|---|---|---|---|---|---|---|

EGR | 1.0000 | |||||

REM | 0.0434657 | 1.0000 | ||||

FDI | -0.052737 | 0.0155788 | 1.0000 | |||

EXR | -0.096110 | 0.633709 | -0.400853 | 1.0000 | ||

GFCF | -0.207263 | -0.776327 | 0.1864522 | -0.609638 | 1.0000 | |

INF | -0.314859 | -0.361168 | 0.4538341 | -0.345601 | 0.3974804 | 1.0000 |

Variables | Levels | Remarks | First Difference | Remarks | ||

|---|---|---|---|---|---|---|

ADF Stats | 5% Crit. Value | ADF Stats | 5% Crit. Value | |||

EGR | -4.0371 | -2.9458 | Stationary | - | - | - |

REM | -1.9099 | -2.9458 | Non-stationary | -6.1761 | -2.9484 | Stationary |

FDI | -3.8143 | -2.9458 | Stationary | - | - | - |

GCFC | -1.6159 | -2.9484 | Non-stationary | -4.8614 | -2.9484 | Stationary |

INF | -3.4793 | -2.9484 | Stationary | - | - | - |

EXR | 2.3719 | -2.9458 | Non-stationary | -4.0451 | -2.9484 | Stationary |

Hypothesized No of CE(s) | EigenValue | Trace Statistics | Prob** | Max-Eigen Statistics | Prob** |

|---|---|---|---|---|---|

None* | 0.828471 | 133.9166 | 0.0000 | 61.70510 | 0.0001 |

At most 1* | 0.667193 | 72.21148 | 0.0318 | 38.50669 | 0.0130 |

At most 2 | 0.376512 | 33.70479 | 0.5180 | 16.53491 | 0.6200 |

At most 3 | 0.260699 | 17.16988 | 0.6275 | 10.57174 | 0.6898 |

At most 4 | 0.121207 | 6.598137 | 0.6248 | 4.522219 | 0.8005 |

At most 5 | 0.057587 | 2.075918 | 0.1496 | 2.075918 | 0.1496 |

Error Correction: | D(EGR) | D(REM) | D(FDI) | D(EXR) | D(GFCF) | D(INF) |

|---|---|---|---|---|---|---|

CointEq1 | -0.550788 | -0.003076 | -0.061623 | -1.224976 | 0.098009 | -2.040006 |

(0.13600) | (0.05304) | (0.04404) | (0.63728) | (0.11950) | (0.35635) | |

[-4.04991] | [-3.05800] | [-3.39910] | [-2.92220] | [1.82015] | [-5.72467] | |

D(EGR(-1)) | 0.499165 | 0.018774 | 0.124559 | 1.678133 | 0.145309 | 0.762380 |

(0.17888) | (0.06977) | (0.05793) | (0.83822) | (0.15718) | (0.46872) | |

[2.79053] | [0.26909] | [2.15017] | [2.00202] | [0.92447] | [1.62652] | |

D(REM(-1)) | -0.686073 | -0.028408 | 0.207826 | -1.332631 | 0.197781 | -0.419196 |

(0.54159) | (0.21124) | (0.17540) | (2.53790) | (0.47590) | (1.41914) | |

[-1.26677] | [-0.13448] | [1.18485] | [-0.52509] | [0.41559] | [-0.29539] | |

D(FDI(-1)) | 1.682313 | -0.116654 | 0.526749 | -5.546782 | -0.230310 | 2.811123 |

(0.58451) | (0.22799) | (0.18930) | (2.73903) | (0.51362) | (1.53161) | |

[2.87816] | [-0.51168] | [2.78262] | [-2.02509] | [-0.44841] | [1.83540] | |

D(EXR(-1)) | 0.114493 | 0.034817 | -0.037739 | 0.472939 | 0.004579 | -0.209595 |

(0.03961) | (0.01545) | (0.01283) | (0.18562) | (0.03481) | (0.10379) | |

[2.89051] | [2.25358] | [-2.94152] | [2.54789] | [0.13156] | [-2.01935] | |

D(GFCF(-1)) | 0.511351 | -0.014470 | 0.271502 | 2.071982 | 0.422658 | -2.329934 |

(0.22557) | (0.08798) | (0.07305) | (1.05702) | (0.19821) | (0.59106) | |

[2.26693] | [-0.16446] | [3.71662] | [1.96021] | [2.13237] | [-3.94193] | |

D(INF(-1)) | -1.185463 | 0.053482 | 0.046036 | 0.482645 | 0.125513 | 0.215631 |

(0.05449) | (0.02125) | (0.01765) | (0.25535) | (0.04788) | (0.14279) | |

[-2.17556] | [2.51680] | [2.60852] | [1.89011] | [2.62142] | [1.51014] | |

C | -0.309908 | 0.698075 | 0.026969 | 12.23346 | -0.392979 | 1.027193 |

(0.81021) | (0.31602) | (0.26240) | (3.79665) | (0.71194) | (2.12301) | |

[-0.38250] | [2.20897] | [0.10278] | [3.22217] | [-0.55198] | [0.48384] | |

R-squared | 0.769749 | 0.442588 | 0.555332 | 0.560668 | 0.618135 | 0.647175 |

Adj. R-squared | 0.606350 | 0.375630 | 0.488195 | 0.494915 | 0.525430 | 0.555702 |

F-statistic | 2.262866 | 3.171574 | 2.125999 | 2.175940 | 4.076118 | 7.075029 |

Error Correction: | D(REM) | D(FDI) | D(EXR) | D(GFCF) | D(INF) |

|---|---|---|---|---|---|

CointEq1 | 0.496971 | 1.723811 | -0.020203 | -0.230117 | 0.395167 |

(0.39940) | (0.65935) | (0.00950) | (0.06754) | (0.04193) | |

[1.24429] | [2.61441] | [-2.12713] | [-3.40688] | [9.42374] |

Component | Jarque-Bera | Df | Prob. |

|---|---|---|---|

1 | 1.352341 | 2 | 0.5086 |

2 | 14.06508 | 2 | 0.0009 |

3 | 1.525494 | 2 | 0.4664 |

4 | 1.153915 | 2 | 0.5616 |

5 | 1.891290 | 2 | 0.3884 |

6 | 0.449933 | 2 | 0.7985 |

Joint | 20.43805 | 12 | 0.0692 |

VEC Residual Serial Correlation LM Tests | ||||||

|---|---|---|---|---|---|---|

Lag | LRE* stat | Df | Prob. | Rao F-stat | Df | Prob. |

1 | 41.11124 | 36 | 0.2566 | 1.152841 | (36, 24.7) | 0.3605 |

2 | 41.62426 | 36 | 0.2392 | 1.175601 | (36, 24.7) | 0.3413 |

3 | 29.94033 | 36 | 0.7514 | 0.720719 | (36, 24.7) | 0.8184 |

Joint test: | ||

|---|---|---|

Chi-sq | Df | Prob. |

548.3932 | 546 | 0.4632 |

ARDL | Autoregressive Distributed Lag |

FDI | Foreign Direct Investment |

DOLS | Dynamic Ordinary Least Squares |

FMOLS | Fully Modified Ordinary Least Squares |

GMM | Generalized Moments of Motions |

GDP | Gross Domestic Product |

ODA | Official Development Assistance |

VAR | Vector Autoregression |

VECM | Vector Autoregressive Distributed Lag |

| [1] | Adeleye, O. K., Ologunwa, O. P., & Ogunjobi, V. O. (2021) Foreign Direct Investment, Remittances and Economic Growth in Nigeria. Do These Inflows Stimulate Growth? Global Journal of Arts, Humanities and Social Sciences, 9(2): 72-82. |

| [2] | Adeseye, A. (2021). The Effect of Migrants Remittance on Economy Growth in Nigeria: An Empirical Study, Open Journal of Political Science, 11, 99-122. |

| [3] | Akter, S. (2016). Remittance inflows and its contribution to the economic growth of Bangladesh. The Journal of Modern Society and Culture, 6(2), 14-28. |

| [4] | Anetor, F. O. (2019). Remittance and economic growth nexus in Nigeria: Does financial sector Development Play a Critical Role? International Journal of Management, Economics and Social Sciences, 8(2), 116 – 135. |

| [5] | Azman-Saini, W. N. W., Law, S. H., & Ahmed, H. A. (2010). Foreign direct investment and economic growth: New evidence on the role of financial markets. Economic Letters, 107(2), 211-213. |

| [6] | Belesity B. A (2022). The impact of foreign financial inflows on the economic growth of sub-Saharan African countries: An empirical approach, Cogent Economics & Finance, 10(1) 21-31. |

| [7] | Bollers, E., & Pile, D (2016). the Nexus between Remittances and Economic Growth: Empirical Evidence from Guyana. Guyana. Journal of International Economics, 115-135. |

| [8] | Chami, R., Fullenkamp, C., & Jahjah, S. (2003). Are immigrant remittance flows a source of capital for development? IMF Working Paper, (189). |

| [9] | Ferdaous, J. (2016). Impact of Remittances and FDI on Economic Growth: A Panel Data Analysis. Journal of Business Studies, 8(2), 16-32. |

| [10] | Goschin, Z. (2014). Remittance as an economic development factor: empirical evidence from the CEE countries. ScienceDirect, Procedia Economics & Finance, 5(10), 54-60. |

| [11] | Iheke, O. (2012). The effect of remittances on the Nigerian economy. International Journal of Development and Sustainability, 12(4), 614-621. |

| [12] | Jushi E., Eglantina H., Arjona C., Mirela P., & Marian C. V. (2021) Financing Growth through Remittances and Foreign Direct Investment: Evidences from Balkan Countries. Journal of Risk and Financial Management, 14(3), 93-117. |

| [13] | Kaphle, R. R. (2019). Relationship between Remittance and Economic Growth in Nepal. Tribhuvan University Journal, 32(2), 249–266. |

| [14] | Karagoz, K. (2009). Workers’ remittances and economic growth: Evidence from Turkey. Journal of Yasar. University, 4(13), 1891-1908. |

| [15] | Keshmeer K., M (2018) Imports, remittances, direct foreign investment and economic growth in Republic of the Fiji Islands: An empirical analysis using ARDL approach, Kasetsart Journal of Social Sciences, 39(1), 439-447. |

| [16] | Khatir, A. & Guvenek, B. (2021). The Effects of FDI and Remittances on the Economic Growth of Selected SAARC Countries. İktisadi ve İdari Yaklaşımlar Dergisi, 3(2), 66-76. |

| [17] | Mamun, Al and Kabir, M. H (2023) "The Remittance, Foreign Direct Investment, Export, and Economic Growth in Bangladesh: A Time Series Analysis," Arab Economic and Business Journal, 15(4), 54-70. |

| [18] | Melnyk, L., Kubatko, O., & Pysarenko, S. (2014). The Impact of Foreign Direct Investment on Economic Growth: Case of Post Communism Transition Economies. Problems and Perspectives in Management, 12(1), 3-12. |

| [19] | Meyer, D. & Shera, A. (2017). The impact of remittance on economic growth: an econometric model. Science Direct, Economic Review, 7(18), 147-155. |

| [20] | Narayan, P. K., & Smyth, R. (2004). Trade liberalization and economic growth in Fiji an empirical assessment using the ARDL approach. Journal of the Asia Pacific Economy, 10(1), 96-115. |

| [21] | Nguyen, N. (2020). The long run and short run impacts of foreign direct investment and export on economic growth of Vietnam, Asian Economic and Financial Review, 7(5), 519-527. |

| [22] | Ola, A. E. (2015). Remittances and economic growth: Empirical evidence from Nigeria and Sri Lanka. Journal of Education Research and Review, 4(5): 91-97. |

| [23] | Olusanya, S. O. (2013). Impact of Foreign Direct Investment Inflow on Economic Growth in a Pre and Post Deregulated Nigeria Economy. A Granger Causality Test. European Scientific Journal, 9(5), 48-63. |

| [24] | Olusanya, S. O., & Olumuyi, O. (2013). Impact of Foreign Direct Investment Inflow on Economic Growth in a Pre and Post Deregulated Nigeria Economy: A Granger Causality Test (1970–2010). European Scientific Journal, 9(25), 335–356. |

| [25] | Omoniyi, O. B., & Owoeye, T. (2024). Effect of Remittance Inflow on Economic Growth of Nigeria. Journal of Applied and Theoretical Social Sciences, 6(1), 74-87. |

| [26] | Osei-Gyebi, S. Opoku, A., Lipede, M. O. and Kountchou, L. K. (2023). The effect of remittance inflow on savings in Nigeria: The role of financial inclusion. Cogent Social Sciences, 9(1), 1-11. |

| [27] | Oshota, S. O., & Badejo A. (2015). The Impact of Remittances on Economic Growth in Nigeria: An Error Correction Modeling Approach; Zagreb International Review of Economics & Business, 6(4), 28-39. |

| [28] | Topxhiu, R., & Xhelili, F. (2016). The role of migrant workers remittances in fostering economic growth: the Kosovo experience. The Romanian Economic Journal, 19(61), 548-604. |

| [29] | Uprety, D. (2017). The impact of remittances on economic growth in Nepal. Journal of Development Innovations, 52(1), 114-134. |

| [30] |

World Bank. (2013). Developing countries to receive over $410 billion in remittances in 2013. Retrieved may 10, 2015, from

http://www.worldbank.org/en/news/pressrelease/2013/10/02/developing-countries-remittances |

| [31] | Zardoub, A. and Sboui, F. (2023), "Impact of foreign direct investment, remittances and official development assistance on economic growth: panel data approach", PSU Research Review, Vol. 7 No. 2, pp. 73-89. |

APA Style

Okungbowa, E. F., Oleabhiele, E. J. (2025). An Examination of the Interrelationship Among Remittance Inflows, Foreign Direct Investment and Economic Growth in Nigeria. International Journal of Economic Behavior and Organization, 13(2), 74-85. https://doi.org/10.11648/j.ijebo.20251302.12

ACS Style

Okungbowa, E. F.; Oleabhiele, E. J. An Examination of the Interrelationship Among Remittance Inflows, Foreign Direct Investment and Economic Growth in Nigeria. Int. J. Econ. Behav. Organ. 2025, 13(2), 74-85. doi: 10.11648/j.ijebo.20251302.12

@article{10.11648/j.ijebo.20251302.12,

author = {Ewere Florence Okungbowa and Eguonor Jennifer Oleabhiele},

title = {An Examination of the Interrelationship Among Remittance Inflows, Foreign Direct Investment and Economic Growth in Nigeria

},

journal = {International Journal of Economic Behavior and Organization},

volume = {13},

number = {2},

pages = {74-85},

doi = {10.11648/j.ijebo.20251302.12},

url = {https://doi.org/10.11648/j.ijebo.20251302.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijebo.20251302.12},

abstract = {The globalization of the world economy, coupled with the recent rise of anti-globalization sentiments in some regions, has made it challenging for underdeveloped nations like Nigeria to fully understand the drivers of economic growth. After gaining independence, Nigeria, like many other growing economies in sub-Saharan Africa, has been striving to achieve and sustain long-term economic growth. The recent downturn in FDI can be attributed to recurring political instability, sluggish economic growth, and a weak global economy, leading to dwindling investment in manufacturing and related sectors. Consequently, examining the long-term relationship between remittances, FDI, and economic growth is crucial for policymakers and government advisers. The present study sought to appraise the relationship among remittance inflow, foreign direct investment (FDI), and economic growth in Nigeria. Time series data, which spanned the period of 1986-2022, was utilized. The vector error correction model was employed for the estimation. From the study, remittance was found to have a negative and non-significant relationship with economic growth. A bi-directional causation was established between FDI and economic growth. Lastly, remittance had no significant relationship with foreign direct investment. The study hence recommends that policymakers should draw up sufficient FDI inflow strategies that would translate to economic growth. This could be done through building confidence in the domestic economy through political stability and cooperation with relevant stakeholders.

},

year = {2025}

}

TY - JOUR T1 - An Examination of the Interrelationship Among Remittance Inflows, Foreign Direct Investment and Economic Growth in Nigeria AU - Ewere Florence Okungbowa AU - Eguonor Jennifer Oleabhiele Y1 - 2025/06/20 PY - 2025 N1 - https://doi.org/10.11648/j.ijebo.20251302.12 DO - 10.11648/j.ijebo.20251302.12 T2 - International Journal of Economic Behavior and Organization JF - International Journal of Economic Behavior and Organization JO - International Journal of Economic Behavior and Organization SP - 74 EP - 85 PB - Science Publishing Group SN - 2328-7616 UR - https://doi.org/10.11648/j.ijebo.20251302.12 AB - The globalization of the world economy, coupled with the recent rise of anti-globalization sentiments in some regions, has made it challenging for underdeveloped nations like Nigeria to fully understand the drivers of economic growth. After gaining independence, Nigeria, like many other growing economies in sub-Saharan Africa, has been striving to achieve and sustain long-term economic growth. The recent downturn in FDI can be attributed to recurring political instability, sluggish economic growth, and a weak global economy, leading to dwindling investment in manufacturing and related sectors. Consequently, examining the long-term relationship between remittances, FDI, and economic growth is crucial for policymakers and government advisers. The present study sought to appraise the relationship among remittance inflow, foreign direct investment (FDI), and economic growth in Nigeria. Time series data, which spanned the period of 1986-2022, was utilized. The vector error correction model was employed for the estimation. From the study, remittance was found to have a negative and non-significant relationship with economic growth. A bi-directional causation was established between FDI and economic growth. Lastly, remittance had no significant relationship with foreign direct investment. The study hence recommends that policymakers should draw up sufficient FDI inflow strategies that would translate to economic growth. This could be done through building confidence in the domestic economy through political stability and cooperation with relevant stakeholders. VL - 13 IS - 2 ER -

Department of Economics, Finance and Investment, Benson Idahosa University, Benin City, Nigeria

Department of Sociology and Anthropology, Benson Idahosa University, Benin City, Nigeria

Information