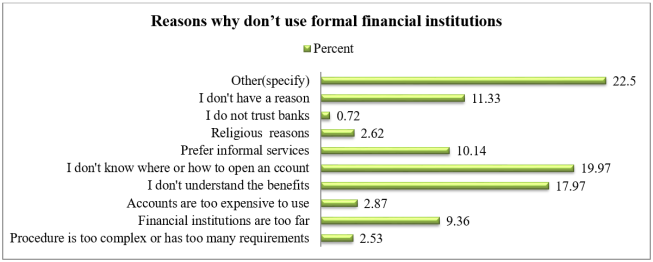

This study examines the relationship between financial inclusion and poverty reduction in Ethiopia, focusing on the barriers to formal financial services faced by households. Using both descriptive and order logit estimation techniques, the research identifies key socioeconomic factors influencing financial exclusion. The study also emphasizes the importance of tailored financial products and inclusive policies to bridge the urban-rural financial gap and ensure equitable economic development. The findings reveal that financial exclusion, driven by both voluntary and involuntary factors, particularly affects the poorest households, limiting their ability to save, invest, and manage risks. While some households voluntarily opt out of formal financial services, involuntary exclusion, caused by factors such as distance, lack of financial literacy, and regulatory barriers, remains more prevalent. The study demonstrates that financial inclusion is positively correlated with improved household economic outcomes and poverty alleviation. It highlights the importance of increasing access to formal financial services, especially in rural areas, reducing transaction costs, and improving financial literacy to empower households to make informed financial decisions. Additionally, the research suggests that enhancing access to affordable credit, particularly for small-scale entrepreneurs and rural households, can foster long-term economic resilience. The study concludes with recommendations for policymakers to create an enabling environment that expands access to financial services and addresses the barriers to financial inclusion, contributing to sustainable poverty reduction in Ethiopia.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 13, Issue 3) |

| DOI | 10.11648/j.ijefm.20251303.13 |

| Page(s) | 93-106 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2025. Published by Science Publishing Group |

Financial Inclusion, Poverty Reduction, Formal Financial Services, Financial Literacy, Ethiopia

Financial institutions | ||

|---|---|---|

The Poor | ||

Apply | Not to apply | |

Provide | ||

Not provide | ||

Name | Label | Description | Expected sign | |

|---|---|---|---|---|

Consumption quintiles in aggregate’s | Within-economy household consumption quintile | Total amount of consumptions per household | ||

Insurance | Insured in the paste | +ve | ||

Account | Has an account | Composite indicator | +ve | |

Modern banking | Use of modern banking services | +ve | ||

Formal Saving account | Saved in the past year | Composite indicator | +ve | |

Credit access | Borrowed in the past 12 months | Composite indicator | +ve | |

Socio economic issues (variables) | ||||

Gender | Respondent is female Sex of the household head: otherwise | 1 if female; 0 otherwise | +ve | |

Age | Respondent age | Age of the household head in years | +ve | |

Education | Respondent education level | highest completed level of education in the family | +ve | |

Shock | Shocks during the last 12 months. | During the last 12 months, was your household affected by shocks? | -ve | |

YES | 1 | |||

NO | 2 | |||

Place of residence | Place where household lives | Rural/urban | ||

Religion | Main religion of household | Orthodox | 1 | |

Catholic | 2 | |||

Protestant | 3 | |||

Muslim | 4 | |||

Traditional | 5 | |||

Pagan | 6 | |||

Wkifata | 7 | |||

Other Specify) | 8 | |||

Marital status | Marital status of household head | Never married | 1 | |

Married (MONOGAMOUS) | 2 | |||

Married (POLYGAMOUS) | 3 | |||

Divorced | 4 | |||

Separated | 5 | |||

Widowed | 6 | |||

Family size | Family size | Household family size | -ve | |

5 Quintiles of Consumption | Have Account | |||||

|---|---|---|---|---|---|---|

Yes | No | Total | ||||

Obs | Freq. | Obs | Freq. | Obs | Freq. | |

Poorest | 78 | 1.71 | 621 | 13.58 | 699 | 15.29 |

Poor | 157 | 3.43 | 620 | 13.56 | 777 | 16.99 |

Average | 189 | 4.13 | 609 | 13.32 | 798 | 17.45 |

Rich | 287 | 6.28 | 627 | 13.71 | 914 | 19.99 |

Richest | 834 | 18.24 | 551 | 12.05 | 1385 | 30.29 |

Total | 1545 | 33.79 | 3028 | 66.21 | 4573 | 100 |

Pearson chi2 (4) = 695.2529 Pr = 0.000 | ||||||

Variable | Obs | Mean | Std.Dev. | Min | Max |

|---|---|---|---|---|---|

Preference of formal financial institution | 4780 | .495 | .5 | 0 | 1 |

Preference of informal financial institution | 4780 | .411 | .492 | 0 | 1 |

Preference of both | 4780 | .094 | .292 | 0 | 1 |

Main reasons of saving | Freq. | Percent | Cum. |

|---|---|---|---|

Emergencies | 1714 | 77.87 | 77.87 |

Health or medical expenses | 45 | 2.04 | 79.92 |

To start or expand a business | 157 | 7.13 | 87.05 |

Old age | 10 | 0.45 | 87.51 |

Education | 26 | 1.18 | 88.69 |

For my children’s future | 55 | 2.50 | 91.19 |

Asset building | 176 | 8.00 | 99.18 |

Other (specify) | 18 | 0.82 | 100.00 |

From Whom Did the HH Member Borrow over the last 12 Months | Freq. | Percent | Cum. |

|---|---|---|---|

Relative | 445 | 41.09 | 41.09 |

Neighbor | 116 | 10.71 | 51.80 |

glossary local merchant | 111 | 10.25 | 62.05 |

Money lender (catapila) | 22 | 2.03 | 64.08 |

Employer | 9 | 0.83 | 64.91 |

religious institution | 39 | 3.6 | 68.51 |

Micro finance institutions | 266 | 24.56 | 93.07 |

Bank (commercial) | 12 | 1.11 | 94.18 |

Ngo | 22 | 2.03 | 96.21 |

Other (specify) | 41 | 3.79 | 100 |

cons_quint | Coef. | St.Err. | Sig |

|---|---|---|---|

Have insurnce | 0.562 | 0.183 | *** |

Being Sav account | 0.139 | 0.071 | * |

Account book | 2.116 | 0.253 | *** |

cradit_yes_no | 0.050 | 0.065 | |

Reside rural 1 | 1.212 | 0.247 | *** |

House hold size | -0.245 | 0.012 | *** |

Vulnerable shock | -0.244 | 0.071 | *** |

Educ head college | -0.078 | 0.131 | * |

Educ head primer | -0.057 | 0.074 | |

Gender | -0.372 | 0.094 | *** |

age_head | -0.019 | 0.003 | *** |

head_married | 0.469 | 0.110 | *** |

Being orthodox | 0.890 | 0.116 | *** |

Being muslim | 1.154 | 0.101 | *** |

Uhat | -16.400 | 1.934 | *** |

Constant | -5.364 | 0.347 | |

Constant | -4.291 | 0.345 | |

Constant | -3.438 | 0.343 | |

Constant | -2.447 | 0.341 | |

Mean dependent var | 3.326 | SD dependent var | 1.446 |

Pseudo r-squared | 0.70 | Number of obs | 4560.000 |

Chi-square | 1010.318 | Prob> chi 2 | 0.000 |

Akaike crit. (AIC) | 13409.872 | Bayesian crit. (BIC) | 13531.948 |

NB *** p<0.01, ** p<0.05, * p<0.1 | |||

Delta-method | ||

|---|---|---|

dy/dx | Std.Err. | |

have_insurnc | ||

_predict | ||

Poorest | 0.073 | 0.024 |

poor | 0.039 | 0.013 |

average | 0.009 | 0.003 |

rich | -0.020 | 0.007 |

richest | -0.100 | 0.033 |

sav_accnt | ||

_predict | ||

Poorest | 0.040 | 0.008 |

poor | 0.022 | 0.004 |

average | 0.005 | 0.001 |

rich | -0.011 | 0.002 |

richest | -0.055 | 0.011 |

accountbook | ||

_predict | ||

Poorest | 0.066 | 0.009 |

poor | 0.035 | 0.005 |

average | 0.008 | 0.001 |

rich | -0.019 | 0.003 |

richest | -0.091 | 0.013 |

cradit_yes_no | ||

_predict | ||

Poorest | 0.005 | 0.008 |

poor | 0.003 | 0.004 |

average | 0.001 | 0.001 |

rich | -0.001 | 0.002 |

richest | -0.007 | 0.010 |

rural 1 | ||

_predict | ||

Poorest | 0.121 | 0.009 |

poor | 0.065 | 0.005 |

average | 0.015 | 0.002 |

rich | -0.034 | 0.003 |

richest | -0.166 | 0.011 |

hh_size | ||

_predict | ||

Poorest | 0.027 | 0.002 |

poor | 0.015 | 0.001 |

average | 0.003 | 0.000 |

rich | -0.008 | 0.001 |

richest | -0.038 | 0.002 |

shock | ||

_predict | ||

Poorest | -0.044 | 0.007 |

poor | -0.024 | 0.004 |

average | -0.005 | 0.001 |

rich | 0.012 | 0.002 |

richest | 0.061 | 0.009 |

educ_hcol | ||

_predict | ||

Poorest | -0.159 | 0.016 |

poor | -0.085 | 0.009 |

average | -0.019 | 0.003 |

rich | 0.045 | 0.006 |

richest | 0.218 | 0.020 |

educ_hprim | ||

_predict | ||

Poorest | -0.034 | 0.007 |

poor | -0.018 | 0.004 |

average | -0.004 | 0.001 |

rich | 0.010 | 0.002 |

richest | 0.047 | 0.010 |

female | ||

_predict | ||

Poorest | -0.025 | 0.010 |

poor | -0.014 | 0.005 |

average | -0.003 | 0.001 |

rich | 0.007 | 0.003 |

richest | 0.035 | 0.014 |

age_head | ||

_predict | ||

Poorest | -0.000 | 0.000 |

poor | -0.000 | 0.000 |

average | -0.000 | 0.000 |

rich | 0.000 | 0.000 |

richest | 0.000 | 0.000 |

head_married | ||

_predict | ||

Poorest | -0.032 | 0.010 |

poor | -0.017 | 0.006 |

average | -0.004 | 0.001 |

rich | 0.009 | 0.003 |

richest | 0.044 | 0.014 |

orthodox | ||

_predict | ||

Poorest | -0.062 | 0.009 |

poor | -0.033 | 0.005 |

average | -0.008 | 0.001 |

rich | 0.017 | 0.003 |

richest | 0.085 | 0.012 |

Muslim | ||

_predict | ||

Poorest | -0.111 | 0.009 |

poor | -0.060 | 0.005 |

average | -0.013 | 0.002 |

rich | 0.031 | 0.003 |

richest | 0.153 | 0.013 |

Source, Own computation from (LSMS &ESS 2015/16) | ||

FI | Financial Inclusion |

CBHI | Community-Based Health Insurance |

SHI | Social Health Insurance |

OOP | Out-of-Pocket (Expenditure) |

CHE | Catastrophic Health Expenditure |

GDP | Gross Domestic Product |

MFIs | Microfinance Institutions |

ATM | Automated Teller Machine |

UNDP | United Nations Development Programme |

NBE | National Bank of Ethiopia |

CSA | Central Statistical Authority |

SDGs | Sustainable Development Goals |

Findex | Global Financial Inclusion Index |

| [1] | Agresti, A. (2002). Logistic regression. Categorical data analysis. |

| [2] | Alemayehu, g., Abebe, S., & Daniel, Z. (2006). Finance and Poverty in Ethiopia Research Paper No.2006/51. |

| [3] | Archer, K. J., & Lemeshow, S. (2006). Goodness-of-fit test for a logistic regression model fitted using survey sample data. The Stata Journal, 6(1), 97-105. |

| [4] | Bannier, C. and Neubert, M. (2016). Actual and perceived financial sophistication and wealth accumulation: the role of education and gender. |

| [5] | Baza, A. U., & Rao, K. S. (2017). Financial inclusion in Ethiopia. International Journal of Economics and Finance, 9(4), 191-201. |

| [6] | Beck, T., & Demirgüç-Kunt, A. (2008). Access to finance: An unfinished agenda. The world bank economic review, 22(3), 383-396. |

| [7] | Behrman, J., Mitchell, O., Soo, C., & Bravo, D. (2012). How financial literacy affects household wealth accumulation. American Economic Review, 102(3), 300-304. |

| [8] | Berhanu Lakew, T., & Azadi, H. (2020, May 2). Financial Inclusion in Ethiopia: Is It on the Right Track? International Journal of Financial Studies, 8(2) 28. |

| [9] | Birhanu, T. (2019). The effect of financial inclusion on household income in Ethiopia. In Addis Ababa University School of Graduate Studies, Addis Ababa University School of Graduate Studies. |

| [10] | Boukhatem, J. (2016). Assessing the direct effect of financial development on poverty reduction in a panel of low-and middle-income countries. Research in International Business and Finance, 37. |

| [11] | Chen, Z., & Jin, M. (2017). Financial inclusion in China: Use of credit. Journal of Family and Economic Issues, 38, 528-540. |

| [12] | Demirguc-Kunt, A., & Levine, R. (2008). Finance and economic opportunity. Washington, DC: World Bank. |

| [13] | Demirgüç-Kunt, A., Klapper, L. F., Singer, D., & Van Oudheusden. The global findex database 2014: Measuring financial inclusion around the world. World Bank Policy Research Working Paper, (7255). |

| [14] | Desalegn, G., & Yemataw, G. (2017). Financial inclusion in Ethiopia: Using LSMS (Ethiopia socioeconomic survey) data. Ethiopian Journal of Economics, 26(2), 31-58. |

| [15] | Dhrifi, A. (2015). Financial development and the" Growth-Inequality-Poverty" triangle. Journal of the Knowledge Economy, 6(4), 1163-1176. |

| [16] | Fungáčová, Z., & Weill, L. (2015). Understanding financial inclusion in China. China Economic Review, 34, 196-206. |

| [17] | Geda, Alemayehu; Shimeles, Abebe; Zerfu, Daniel (2006): Finance and poverty in Ethiopia: A household level analysis, WIDER Research Paper, No. 2006/51, ISBN 9291908193. |

| [18] | Hasan, I., Horváth, R., & Mareš, J. (2020). Finance and wealth inequality. Journal of International Money and Finance, 108, 102161. |

| [19] | Hudson, C. and Young, J. (2022). Wealth: factors that affect African American wealth. The Review of Black Political Economy, 50(1), 97-116. |

| [20] | Jakobsen, K. T. (2011). Determinants of welfare dynamics in rural Nicaragua. The European Journal of Development Research, 23, 371-388. |

| [21] | Kama, U., & Adigun, M. (2013). Financial inclusion in Nigeria: Available at SSRN 2365209. |

| [22] | Khalid, U., Shahnaz, L., & Bibi, H. (2005). Determinants of poverty in Pakistan: A multinomial logit approach. The Lahore Journal of Economics, 10(1), 65-81. |

| [23] | Kingsley, C. M. (2013). A global view on financial inclusion: perspectives from a frontier market. |

| [24] | Lashley, J. G. (2004). Microfinance and Poverty Alleviation in the Caribbean: A Strategic Overview. Journal of Microfinance/ESR Review, 6(1), 6. |

| [25] | Liu, Y., Zhao, H., Sun, J., & Tang, Y. (2022). Digital inclusive finance and family wealth: evidence from lightapproach. Sustainability, 14(22), 15363. |

| [26] | Martinetti, E. C. (1994). A new approach to evaluation of well-being and poverty by fuzzy set theory. Giornale degli economisti e annali di economia, 367-388. |

| [27] | Rahadi, R., Danella, J., & Okdinawati, L. (2019). The correlation between financial literacy and family wealth distribution in bandung. |

| [28] | Wang, S., Guo, Y., & He, Z. (2023). Analysis on the measurement and dynamic evolution of multidimensional return to poverty in Chinese rural households, 165(1). |

| [29] | Zins, A., & Weill, L. (2016). The determinants of financial inclusion in Africa. Review of development finance, 6(1), 46-57. |

APA Style

Abate, T. M. (2025). Contribution of Financial Inclusion to Poverty Reduction in Ethiopia. International Journal of Economics, Finance and Management Sciences, 13(3), 93-106. https://doi.org/10.11648/j.ijefm.20251303.13

ACS Style

Abate, T. M. Contribution of Financial Inclusion to Poverty Reduction in Ethiopia. Int. J. Econ. Finance Manag. Sci. 2025, 13(3), 93-106. doi: 10.11648/j.ijefm.20251303.13

@article{10.11648/j.ijefm.20251303.13,

author = {Teshome Mihret Abate},

title = {Contribution of Financial Inclusion to Poverty Reduction in Ethiopia

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {13},

number = {3},

pages = {93-106},

doi = {10.11648/j.ijefm.20251303.13},

url = {https://doi.org/10.11648/j.ijefm.20251303.13},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20251303.13},

abstract = {This study examines the relationship between financial inclusion and poverty reduction in Ethiopia, focusing on the barriers to formal financial services faced by households. Using both descriptive and order logit estimation techniques, the research identifies key socioeconomic factors influencing financial exclusion. The study also emphasizes the importance of tailored financial products and inclusive policies to bridge the urban-rural financial gap and ensure equitable economic development. The findings reveal that financial exclusion, driven by both voluntary and involuntary factors, particularly affects the poorest households, limiting their ability to save, invest, and manage risks. While some households voluntarily opt out of formal financial services, involuntary exclusion, caused by factors such as distance, lack of financial literacy, and regulatory barriers, remains more prevalent. The study demonstrates that financial inclusion is positively correlated with improved household economic outcomes and poverty alleviation. It highlights the importance of increasing access to formal financial services, especially in rural areas, reducing transaction costs, and improving financial literacy to empower households to make informed financial decisions. Additionally, the research suggests that enhancing access to affordable credit, particularly for small-scale entrepreneurs and rural households, can foster long-term economic resilience. The study concludes with recommendations for policymakers to create an enabling environment that expands access to financial services and addresses the barriers to financial inclusion, contributing to sustainable poverty reduction in Ethiopia.

},

year = {2025}

}

TY - JOUR T1 - Contribution of Financial Inclusion to Poverty Reduction in Ethiopia AU - Teshome Mihret Abate Y1 - 2025/06/18 PY - 2025 N1 - https://doi.org/10.11648/j.ijefm.20251303.13 DO - 10.11648/j.ijefm.20251303.13 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 93 EP - 106 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20251303.13 AB - This study examines the relationship between financial inclusion and poverty reduction in Ethiopia, focusing on the barriers to formal financial services faced by households. Using both descriptive and order logit estimation techniques, the research identifies key socioeconomic factors influencing financial exclusion. The study also emphasizes the importance of tailored financial products and inclusive policies to bridge the urban-rural financial gap and ensure equitable economic development. The findings reveal that financial exclusion, driven by both voluntary and involuntary factors, particularly affects the poorest households, limiting their ability to save, invest, and manage risks. While some households voluntarily opt out of formal financial services, involuntary exclusion, caused by factors such as distance, lack of financial literacy, and regulatory barriers, remains more prevalent. The study demonstrates that financial inclusion is positively correlated with improved household economic outcomes and poverty alleviation. It highlights the importance of increasing access to formal financial services, especially in rural areas, reducing transaction costs, and improving financial literacy to empower households to make informed financial decisions. Additionally, the research suggests that enhancing access to affordable credit, particularly for small-scale entrepreneurs and rural households, can foster long-term economic resilience. The study concludes with recommendations for policymakers to create an enabling environment that expands access to financial services and addresses the barriers to financial inclusion, contributing to sustainable poverty reduction in Ethiopia. VL - 13 IS - 3 ER -

Department of Economics, College of Business and Economics, Debre Markos University, Debre Markos, Ethiopia

Information