2. Literature Review

2.1. Concept of Audit

Audit is a systematic and independent examination of an organization's financial statements, records, operations, and processes to assess their accuracy, reliability, and compliance with applicable laws, regulations, and internal policies. The objective of an audit is to provide assurance to stakeholders, such as shareholders, investors, and regulators, regarding the financial health and integrity of the organization.

2.2. Internal Audit

Internal auditing is a crucial function within organizations that aims to enhance operations by providing an independent and objective assessment of risk management, control, and governance procedures. The Institute of Internal Auditors (IIA) defines internal auditing as a function that rigorously evaluates and improves the effectiveness of an organization by ensuring the accuracy and reliability of information, identifying and mitigating risks, ensuring regulatory compliance, and optimizing resource utilization

| [23] | Kanyi, D., & Ragui, M. (2023). Internal Audit and Business Resilience in Power Sector. A Case of Geothermal Development Company. Journal of Strategic Management, 7(2), 50-71. https://doi.org/10.53819/81018102t6055 |

[23]

. These definitions and emphasize the importance of internal auditing in achieving organizational goals

| [12] | Hailemariam, S. (2014). Determinants of internal audit effectiveness in the public sector, case study in selected Ethiopian public sector offices (Doctoral dissertation, Jimma University). |

| [25] | Pickett, K. S. (2010). The Internal Auditing Handbook. John Wiley & Sons, Inc. |

[12, 25]

.

2.3. Types of Internal Audits

Internal audits serve various functions tailored to an organization's unique risk exposures. Four common types of internal audits are operational audits, compliance audits, follow-up audits, and investigative audits. Operational audits evaluate the effectiveness and efficiency of specific organizational departments or functions, providing insights for improvement. Compliance audits ensure adherence to laws, standards, and regulations relevant to the organization's operations. Follow-up audits assess the progress made in addressing previous audit recommendations, ensuring accountability and continuous improvement. Investigative audits focus on verifying suspected cases of fraud or financial irregularities, safeguarding organizational assets

| [25] | Pickett, K. S. (2010). The Internal Auditing Handbook. John Wiley & Sons, Inc. |

[25]

.

2.4. Role of Internal Audit

The role of internal audit extends beyond the traditional evaluation of financial statements. Internal auditors play a crucial role in assessing compliance functions, evaluating internal control systems, and scrutinizing operational areas. They establish accountability, analyze previous audit findings, and contribute to the overall improvement of organizational processes. Internal auditors also create long-term audit plans, identifying areas of risk and opportunity for increased efficiency and effectiveness. Their role is essential in providing assurance to management and stakeholders regarding the organization's risk management, control, and governance processes

| [23] | Kanyi, D., & Ragui, M. (2023). Internal Audit and Business Resilience in Power Sector. A Case of Geothermal Development Company. Journal of Strategic Management, 7(2), 50-71. https://doi.org/10.53819/81018102t6055 |

| [25] | Pickett, K. S. (2010). The Internal Auditing Handbook. John Wiley & Sons, Inc. |

[23, 25]

.

2.5. Internal Audit Effectiveness (IAE)

Internal audit effectiveness refers to the achievement of predetermined goals and the value added by the internal audit function. It involves assessing the key elements that contribute to internal audit effectiveness and evaluating whether outcomes align with objectives. Several factors influence internal audit effectiveness, including the organizational setting, independence and objectivity of internal auditors, competency of internal audit staff, management support, and the nature and scope of internal audit activities. Understanding these factors and their impact on internal audit effectiveness is crucial for organizations to optimize their internal audit function and enhance overall organizational performance

| [25] | Pickett, K. S. (2010). The Internal Auditing Handbook. John Wiley & Sons, Inc. |

[25]

.

2.6. Independence of Internal Audit and Internal Audit Effectiveness

For example, a survey-based study conducted and found that internal auditors who perceived higher levels of independence reported greater effectiveness in their audit activities

| [15] | Kamara, A. K. (2023). An Assessment of the Effectiveness of the Internal Audit on the Performance of the Public Sector: Case Study of the National Revenue Authority (NRA). 10. https://doi.org/10.4236/oalib.1110432 |

[15].

Similarly, the impact of actual independence, measured by factors such as reporting lines and organizational structure, and found a positive relationship with internal audit effectiveness

| [24] | Pham, D. C., & Nguyen, T. T. (2021). Factors affecting the internal audit effectiveness of steel enterprises in Vietnam. The Journal of Asian Finance, Economics and Business, 8(1), 271-283. |

[24]

. Additionally

| [11] | Gramling, A., & Schneider, A. (2018). Effects of reporting relationship and type of internal control deficiency on internal auditors’ internal control evaluations. Managerial Auditing Journal, 33(3), 318-335. |

[11]

found that greater internal audit independence led to improved detection and prevention of financial statement errors in publicly traded companies. In the context of governmental organizations,

| [22] | Oladejo, M., Yinus, S. O., Shittu, S., &Rutaro, A. (2021). Internal audit practice and financial reporting quality: Perspective from Nigerian quoted foods and beverages firms. KIU Interdisciplinary Journal of Humanities and Social Sciences, 2(1), 410-428. |

| [30] | Yemataw, S. D. (2022). Determinants of Internal Audit Effectiveness: The Case of Berhan Bank Sc and Abay Bank Sc (Doctoral Dissertation, Addis Ababa University). |

[22, 30]

found that perceived independence positively influenced compliance with laws and regulations, as well as the quality of audit reports.

2.7. Top Management Support and Internal Audit Effectiveness

For instance,

| [14] | Iyer, V. M., Jones III, A., &Raghunandan, K. (2018). Factors related to internal auditors' organizational-professional conflict. Accounting Horizons, 32(4), 133-146. |

[14]

conducted a quantitative study of organizations across different industries and found that higher levels of top management support were associated with greater internal audit effectiveness. Similarly,

| [5] | Brown, T., & Fanning, K. (2019). The joint effects of internal auditors' approach and persuasion tactics on managers' responses to internal audit advice. The Accounting Review, 94(4), 173-188. |

| [13] | Saddam A. Hazaea, Mosab I. Tabash, Jinyu Zhu, Saleh F. A. Khatib and Najib H. S. Farhan (2021). Internal audit and financial performance of Yemeni commercial banks: Empirical evidence. Banks and Bank Systems, 16(2), 137-147. https://doi.org/10.21511/bbs.16(2).2021.13 |

[5, 13]

conducted a survey-based study and observed that internal auditors perceived higher levels of support from top management positively influenced their effectiveness in risk assessment and control testing. In addition top management support significantly influences internal audit effectiveness.

| [6] | Chen, Y., Lin, B., Lu, L., & Zhou, G. (2020). Can internal audit functions improve firm operational efficiency? Evidence from China. Managerial Auditing Journal, 35(8), 1167-1188. |

[6]

found that active support and promotion from top management improves risk identification, control evaluation, and overall effectiveness of internal audits. Similarly,

| [1] | Alkebsi, M., & Aziz, K. A. (2017). Information technology usage, top management support and internal audit effectiveness. Asian Journal of Accounting and Governance, 8(1), 123-132. |

[1]

observed a positive relationship between top management support and the perceived effectiveness of internal audit functions in emphasizing the function's ability to provide valuable insights and recommendations.

2.8. Organizational Setting and Internal Audit Effectiveness

The studies highlight variations in internal audit effectiveness across different organizational settings. They suggest that factors such as the complexity of the organizational structure, regulatory environment, and stakeholder expectations can significantly impact internal audit effectiveness. Furthermore,

| [3] | Azzali, S., &Mazza, T. (2018). The internal audit effectiveness evaluated with an organizational, process and relationship perspective. International Journal of Business and Management, 13(6), 238-254. |

[3]

compared internal audit effectiveness in public and private sector organizations in China and found higher effectiveness in private companies attributed to their greater flexibility and less bureaucratic nature.

| [27] | Roussy, M., Barbe, O., & Raimbault, S. (2020). Internal audit: from effectiveness to organizational significance. Managerial Auditing Journal, 35(2), 322-342. |

[27]

highlighted that factors such as strong governance structures, active board involvement, and adequate resources positively influenced internal audit effectiveness in nonprofit organizations.

The study by

| [30] | Yemataw, S. D. (2022). Determinants of Internal Audit Effectiveness: The Case of Berhan Bank Sc and Abay Bank Sc (Doctoral Dissertation, Addis Ababa University). |

[30]

conducted a comparative study of internal audit effectiveness in public and private organizations and found that public sector internal audit functions faced greater challenges in achieving effectiveness due to bureaucratic structures and political influences. On the other hand, research by

| [2] | Alqudah, H. M., Amran, N. A., & Hassan, H. (2019). Factors affecting the internal auditors’ effectiveness in the Jordanian public sector: The moderating effect of task complexity. EuroMed Journal of Business, 14(3), 251-273. |

| [16] | Kapri, S. S. (2021). The Role of Corporate Governance in Mitigating Financial Risk: An Indian Experiences. Journal of Cardiovascular Disease Research, 2(6) https://doi.org/10.48047/jcdr.2021.12.06.329 |

[2, 16]

examined internal audit effectiveness in nonprofit organizations and observed that factors such as resource constraints and board governance influenced effectiveness.

2.9. Audit Committee and Internal Audit Effectiveness

A study conducted a quantitative study and found that a higher level of audit committee effectiveness, as perceived by internal auditors, was positively associated with internal audit effectiveness

| [5] | Brown, T., & Fanning, K. (2019). The joint effects of internal auditors' approach and persuasion tactics on managers' responses to internal audit advice. The Accounting Review, 94(4), 173-188. |

[5]

. Similarly,

| [14] | Iyer, V. M., Jones III, A., &Raghunandan, K. (2018). Factors related to internal auditors' organizational-professional conflict. Accounting Horizons, 32(4), 133-146. |

| [20] | Mohammed, A., Shuwaili, J., &Hesarzadeh, R. (2022). Designing an internal audit effectiveness model for public sector: qualitative and quantitative evidence from a developing country. https://doi.org/10.1108/JFM-07-2022-0077 |

[14, 20]

examined the impact of the independence of the audit committee and found a positive relationship with internal audit effectiveness. Audit committee characteristics also play a crucial role in internal audit effectiveness. Also

| [19] | Mieseigha, E. G., &Adeyemi, A. A. (2021). Audit committee attributes and firm revenue growth in the Nigerian banking industry. Journal of Advanced Research in Management, 12(2), 47-53. |

| [28] | Salehi, T. (2016). Investigation Factors Affecting the Effectiveness of Internal Auditors in the Company: Case Study Iran. 8(2), 224-235. https://doi.org/10.5539/res.v8n2p224 |

[19, 28]

found a positive relationship between audit committee effectiveness, measured by factors such as expertise, independence, and meetings frequency, and internal audit effectiveness in Nigerian listed companies. In family-controlled firms,

| [28] | Salehi, T. (2016). Investigation Factors Affecting the Effectiveness of Internal Auditors in the Company: Case Study Iran. 8(2), 224-235. https://doi.org/10.5539/res.v8n2p224 |

| [29] | Yahaya, I. D., &Okoroigwe, E. S. (2022). Moderating Effect of Audit Committee Financial Expertise on the Relationship between Audit Quality and Earnings Management of Quoted Consumer Goods Firms in Nigeria. Lapai Journal of Economics, 6(2), 34-48. |

[28, 29]

emphasized that an active and independent audit committee enhances the effectiveness of the internal audit function by ensuring appropriate oversight and support.

2.10. Competency of Internal Auditor and Internal Audit Effectiveness

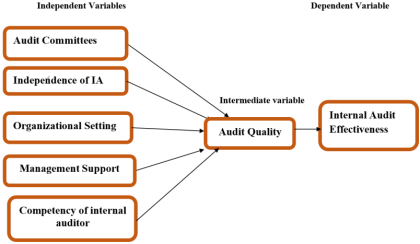

Figure 1. Conceptual Framework.

According to

| [30] | Yemataw, S. D. (2022). Determinants of Internal Audit Effectiveness: The Case of Berhan Bank Sc and Abay Bank Sc (Doctoral Dissertation, Addis Ababa University). |

[30]

study found that the presence of adequate and competent internal audit staff is positively related to internal audit effectiveness (IAE). This suggests that when internal auditors possess the necessary skills and expertise, they are more likely to contribute significantly to the effectiveness of internal audit. The study further highlights that competent internal auditors are able to perform their activities on time, which further enhances the overall effectiveness of internal audit.

Similarly,

| [9] | George, D., Theofanis, K., &Konstantinos, A. (2015). Factors associated with internal audit effectiveness: Evidence from Greece. Journal of Accounting and Taxation, 7(7), 113-122. |

| [17] | Kassie, W. D. (2021). Bank Specific Determinants of Internal Audit Effectiveness: Evidence from Private Banks in Ethiopia. European Journal of Business and Management, 13(5), https://doi.org/10.7176/EJBM/13-5-0 |

[9, 17]

also support the notion of a positive relationship between the competency of internal auditors and internal audit effectiveness. While the specific details of these studies were not provided, it can be inferred that these researchers found evidence suggesting that when internal auditors possess the required competencies, it leads to improved effectiveness in conducting internal audits.

3. Research Methodology

3.1. Description of the Study Area

The study area for this research is Lemi Kura sub-city, located in the southeastern part of Addis Ababa, the capital city of Ethiopia.

Figure 2. Map of Addis Ababa showing Lemi Kura Sub city.

3.2. Research Design

This study employed an explanatory and descriptive research design to assess the factors affecting the effectiveness of internal audits in the public sectors of Lemikura sub-city, Addis Ababa. The use of an explanatory research design was appropriate as it allowed for a deeper understanding of the causal relationships and factors that influenced internal audit effectiveness within the specific context of Lemikura sub-city.

3.3. Sources and Types of Data

This study primarily relies on the collection of primary data to investigate the factors influencing the effectiveness of internal audits in the public sectors of Lemi Kura Sub City.

This study utilizes quantitative data to investigate the factors influencing the effectiveness of internal audits in the public sectors of Lemi Kura Sub City. The quantitative data are collected through a structured survey questionnaire. The questionnaire comprises items designed to capture the respondents' perceptions of the factors influencing internal audit effectiveness, such as management support, organizational setting, independence, and audit committees. The quantitative data are numerical in nature and are collected using a Likert scale.

3.4. Population and Sampling Frame

The target population for this study consists of senior managers and internal auditors working in the public sectors of Lemikura sub-city, Addis Ababa. The population includes 9 senior managers and 122 internal auditors who are actively involved in internal audit activities within the public sector organizations in the sub-city. The inclusion of senior managers in the target population is crucial as they play a significant role in providing management support and creating an environment conducive to effective internal audits. Their perspectives and insights are essential for understanding the factors that influence internal audit effectiveness, such as resource allocation, organizational structure, and the establishment of audit committees.

This study employed a census approach to include the entire target population of senior managers and internal auditors in the public sectors of Lemikura sub-city, Addis Ababa. A census approach was deemed appropriate for this study as the population size was manageable, consisting of 9 senior managers and 122 internal auditors.

3.5. Model Specifications

Effective audit committee was hypothesized to positively affect IA effectiveness. Active and independent audit committees provided oversight and support to the internal audit function, enhancing its efficiency and effectiveness. Therefore, the audit committee variable was expected to have a positive coefficient in the regression model. The multiple regression models can be expressed as follows:

IAE= β0+β1(TMS) +β2(IIA)+β3(OS)+β4(AC)+ β5(IAC)+ β6(AQ) + ε

Hypothesis

H0: The factors have no significant effect on IA effectiveness.

H1: Top management support (TMS) has statistically significant effect on internal audit effectiveness (IAE).

H2: Independence of internal auditors (IIA) support has statistically significant effect on internal audit effectiveness (IAE).

H3: Organizational setting (OS) has statistically significant effect on internal audit effectiveness (IAE).

H4: The presence of an audit committee (AC) has statistically significant effect on internal audit effectiveness (IAE).

H5: Internal Audit competency (IAC) has significant effect on internal audit effectiveness (IAE).

H6: Audit Quality (AQ) has significant effect on internal audit effectiveness (IAE).

3.6. Reliability

The internal consistency of the questionnaire was assessed using Cronbach's alpha coefficient. This coefficient measured the extent to which the items within each construct of the questionnaire were interrelated and provided consistent measurements. A high Cronbach's alpha value (typically above 0.70) indicated good internal consistency and reliability.

Table 1 below shows the reliability of the questionnaires.

Table 1. Reliability Test.

Reliability Statistics |

Cronbach's Alpha | N of Items |

.935 | 7 |

Source: Survey April, 2024

4. Results and Discussions

4.1. Diagnosis of Ordinary Least Square (OLS) Assumptions

1) Assessment of Normality

Table 2 below shows the Shapiro-Wilk test of normality conducted for the variables internal audit Effectiveness, Top Management Support, Internal Audit Independence, Organizational Setting, and Audit Committee. The results indicate that the data for all variables are likely to follow a normal distribution, as the p-values obtained from the test are greater than the conventional significance level of 0.05.

Table 2. Test of Normality results.

| Shapiro-Wilk |

Statistic | df | Sig. |

IA Effectiveness | .983 | 131 | .090 |

Top Management Support | .981 | 131 | .067 |

IA Independence | .983 | 131 | .096 |

Organizational Setting | .987 | 131 | .239 |

Audit Committee | .987 | 131 | .265 |

Internal Auditors Competency | .986 | 131 | .198 |

Audit Quality | .983 | 131 | .091 |

Source: Field Survey, 2024

2) Assessment of Heteroskedasticity

Table 3 below shows the Breusch-Pagan test for heteroskedasticity conducted to examine whether the variance of errors in the Internal Audit Effectiveness variable is dependent on the values of the independent variables. The test resulted in a chi-square statistic of 0.140 with 1 degree of freedom and a p-value of 0.0.708. Since the p-value is greater than the conventional significance level of 0.05, we fail to reject the null hypothesis, indicating that there is no significant evidence of heteroskedasticity in the Internal Audit Effectiveness variable. This suggests that the variance of errors in Internal Audit Effectiveness does not vary systematically with the values of the independent variables included in the model. Therefore, the assumption of constant variance, known as homoskedasticity, is reasonable for the Internal Audit Effectiveness variable.

Table 3. Test for Heteroskedasticity results.

Modified Breusch-Pagan Test for Heteroskedasticitya, b, c |

Chi-Square | Df | Sig. |

.140 | 1 | .708 |

a. Dependent variable: IA Effectiveness |

b. Tests the null hypothesis that the variance of the errors does not depend on the values of the independent variables. |

c. Predicted values from design: Intercept + Mgt Support * Internal Audit Independence * Organizational Setting * Internal Audit Committee * Competency * AuditQuality |

Source: Survey April, 2024

3) Assessment of Multicollinearity

The test for multicollinearity in

Table 4 below examined the correlation among independent variables in predicting Internal Audit Effectiveness. The results indicate that there is no significant multicollinearity issue among the variables as the tolerance values are above 0.1 and the VIF values are below 10. This suggests that the independent variables, including Top Management Support, Internal Audit Independence, Organizational Setting, Audit Committee, Internal Auditors Competency, and Audit Quality, are relatively independent of each other when predicting Internal Audit Effectiveness.

4) Assessment of Autocorrelation

Table 5 presents the results of the test for autocorrelation, specifically displaying the Durbin-Watson statistic. The Durbin-Watson statistic is used to detect the presence of autocorrelation, also known as serial correlation, refers to the correlation of a variable with its own lagged values over time. It is a concern primarily in time series analysis, where observations are collected over consecutive time periods. In cross-sectional data, where observations are collected at a single point in time, the assumption of independence between observations is typically more straightforward to meet. Autocorrelation is not a typical concern in cross-sectional data analysis.

In the given table, the Durbin-Watson statistic is reported as 2.119. This value is close to 2, suggesting that there is no significant autocorrelation present in the model. It implies that the error terms in the regression model are not systematically correlated across observations.

Table 4. Test for Multicollinearity results.

Coefficientsa |

Model | Collinearity Statistics |

Tolerance | VIF |

1 | Top Management Support | .336 | 2.975 |

Internal Audit Independence | .355 | 2.821 |

Organizational Setting | .507 | 1.973 |

Audit Committee | .340 | 2.938 |

Internal Auditors Competency | .222 | 4.515 |

Audit Quality | .399 | 2.509 |

a. Dependent Variable: Internal Audit Effectiveness |

Source: Survey April, 2024

Table 5. Test for Autocorrelation results.

Model Summaryb |

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin-Watson |

1 | .867a | .751 | .739 | .47298 | 2.119 |

a. Predictors: (Constant), Organizational Setting, Audit Quality, Internal Audit Independence, Audit Committee, Top Management Support, Internal auditors Competency |

b. Dependent Variable: Internal Audit Effectiveness |

Source: Survey April, 2024

4.2. Correlation Results

Table 6. Correlation results.

Correlation | IA Effectiveness | IA Quality | Independence | Competency | Mgt Support | Committee | Organizational Setting |

IA Effectiveness | 1 | .685** | .608** | .801** | .642** | .741** | .403** |

IA Quality | .685** | 1 | .486** | .364** | .510** | .537** | .339** |

Independence | .608** | .486** | 1 | .357** | .345** | .486** | .349** |

Competency | .801** | .364** | .357** | 1 | .442** | .363** | .344** |

Mgt Support | .642** | .510** | .345** | .442** | 1 | .209** | .357** |

Committee | .741** | .537** | .486** | .363** | .209** | 1 | .572** |

Organizational Setting | .403** | .339** | .349** | .344** | .357** | .572** | 1 |

Source: Survey April, 2024

Table 6 above shows the correlation relationship among various factors affecting internal audit effectiveness. Notably, Internal Audit effectiveness has the strongest correlation with competency (r = 0.801), indicating that higher auditor competency is crucial for effective audits. Independence (r = 0.698) and committee involvement (r = 0.741) also show strong positive correlations with internal audit effectiveness, suggesting that both are critical in enhancing audit outcomes. Quality (r = 0.685) and management support (r = 0.642) are moderately correlated with effectiveness, highlighting their importance. Organizational setting, though having the weakest significant correlation (r = 0.403), still plays a role. These relationships emphasize that a multifaceted approach, improving various aspects like competency, independence, and committee roles, is essential for effective internal auditing.

4.3. Regression Results

The Model Summary table in

Table 7 below provides the coefficient of determination (R Square) is 0.751, indicating that 75.1% of the variation in the dependent variable (internal audit effectiveness) can be explained by the independent variables included in the model. This suggests that the model has a reasonably good fit, and the selected independent variables collectively have a strong influence on internal audit effectiveness.

Table 7. Model goodness of fit results.

Model Summaryb |

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin-Watson |

1 | .867a | .751 | .739 | .47298 | 2.119 |

a. Predictors: (Constant), Organizational Setting, Audit Quality, Internal Audit Independence, Audit Committee, Top Management Support, Internal auditors Competency |

b. Dependent Variable: IAEffectiveness |

Source: Survey April, 2024

Table 8 below shows the ANOVA gives a highly significant result (F = 59.983, Sig. <.001), thereby indicating that Organizational Setting, Audit Quality, Internal Audit Independence, Audit Committee, Top Management Support, Internal auditors Competency under the study can significantly influence Internal Audit Effectiveness.

Table 8. ANOVA results.

ANOVAa |

Model | Sum of Squares | Df | Mean Square | F | Sig. |

1 | Regression | 83.648 | 6 | 13.941 | 62.319 | .000b |

Residual | 27.740 | 124 | .224 | | |

Total | 111.388 | 130 | | | |

a. Dependent Variable: Internal Audit Effectiveness |

b. Predictors: (Constant), Organizational Setting, Audit Quality, Internal Audit Independence, Audit Committee, Top Management Support, Internal auditors Competency |

Source: Survey April, 2024

The multiple linear regression result that are obtained by regressing the internal audit effectiveness in adding value of top management support, internal audit independence, organizational setting, audit committee, internal auditors competency, and audit quality were analyze and reported. Finally, the hypothesis tests were undertaken based on the proposed hypothesis and the regression output results. The multiple linear regression model for internal audit effectiveness based on the coefficients in

Table 9 below can be expressed as follows:

internal audit effectiveness = -0.632+ 0.186 (Top Management Support) + 0.295 (internal audit Independence) - 0.331 (Organizational Setting) + 0.362 (Audit Committee) + 0.473 (Internal Auditors Competency) + 0.209 (Audit Quality) + ε

Table 9. Regression Results for Internal Audit Effectiveness.

Coefficientsa |

Model | Unstandardized Coefficients | Standardized Coefficients | T | Sig. |

B | Std. Error | Beta |

1 | (Constant) | -.632 | .324 | | -1.949 | .054 |

Top Management Support | .186 | .092 | .157 | 2.030 | .045 |

IA Independence | .295 | .111 | .199 | 2.650 | .009 |

Organizational Setting | -.331 | .098 | -.212 | -3.374 | .001 |

Audit Committee | .362 | .101 | .276 | 3.593 | .000 |

Internal Auditors Competency | .473 | .130 | .346 | 3.629 | .000 |

Audit Quality | .209 | .088 | .168 | 2.372 | .019 |

a. Dependent Variable: IA Effectiveness |

Source: Survey April, 2024

4.3.1. Top Management and Internal Audit Effectiveness

The first objective of the study is to investigate the impact of support from top management on achieving internal audit effectiveness. Based on the multiple linear regression results presented in

Table 9 above, the findings regarding the objective of investigating the impact of support from top management on achieving internal audit effectiveness can be discussed. In the regression results, the variable Top Management Support has a coefficient of 0.186 with a standard error of 0.092. The standardized coefficient (Beta) is 0.157. The t-value for this variable is 2.030, indicating statistical significance at the p < 0.05 level.

The positive coefficient for top management support suggests a positive relationship between top management support and internal audit effectiveness. The effect size is with each unit increase in top management support associated with a 0.186 unit increase in internal audit effectiveness. The standardized coefficient (Beta) indicates that top management support accounts for approximately 15.7% of the variance in internal audit effectiveness.

These findings align with previous empirical evidence supporting the positive impact of top management support on internal audit effectiveness. Studies such as

| [5] | Brown, T., & Fanning, K. (2019). The joint effects of internal auditors' approach and persuasion tactics on managers' responses to internal audit advice. The Accounting Review, 94(4), 173-188. |

| [14] | Iyer, V. M., Jones III, A., &Raghunandan, K. (2018). Factors related to internal auditors' organizational-professional conflict. Accounting Horizons, 32(4), 133-146. |

| [28] | Salehi, T. (2016). Investigation Factors Affecting the Effectiveness of Internal Auditors in the Company: Case Study Iran. 8(2), 224-235. https://doi.org/10.5539/res.v8n2p224 |

[5, 14, 28]

have reported similar positive relationships between top management support and internal audit effectiveness. In general, the regression results indicate a statistically significant positive relationship between top management support and internal audit effectiveness and it is consistent with previous empirical studies.

4.3.2. Independence of Internal Auditors on the Effectiveness of Internal Audit

The second objective of this study is to examine the impact of the independence of internal auditors on the effectiveness of internal audit.

Table 9 shows the regression results of the variable internal audit independence has an unstandardized coefficient of 0.295 with a standard error of 0.111. The associated t-value is 2.650, indicating that the coefficient is statistically significant at the 0.05 level (p = 0.009).

The positive coefficient indicates a positive relationship between IA independence and internal audit effectiveness. Specifically, an increase in IA independence by one unit is associated with a 0.295 unit increase in internal audit effectiveness. The standardized coefficient (Beta) of 0.199 further supports this relationship, suggesting that IA independence explains approximately 19.9% of the variance in internal audit effectiveness.

The findings align with previous empirical evidence, which consistently supports the positive association between independence and internal audit effectiveness. For instance, studies conducted by

| [18] | Massawe, A. D. F. (2020). Determinants of Internal Audit Function Effectiveness of DSE Listed Companies in Tanzania: Moderation Effect of Audit Committee (Doctoral dissertation, The Open University of Tanzania). |

| [24] | Pham, D. C., & Nguyen, T. T. (2021). Factors affecting the internal audit effectiveness of steel enterprises in Vietnam. The Journal of Asian Finance, Economics and Business, 8(1), 271-283. |

[18, 24]

have found that perceived and actual independence of internal auditors contribute to greater effectiveness in audit activities. Additionally,

| [11] | Gramling, A., & Schneider, A. (2018). Effects of reporting relationship and type of internal control deficiency on internal auditors’ internal control evaluations. Managerial Auditing Journal, 33(3), 318-335. |

[11]

reported that greater internal audit independence leads to improved detection and prevention of financial errors in publicly traded companies. Moreover, research conducted in the context of governmental organizations by

| [22] | Oladejo, M., Yinus, S. O., Shittu, S., &Rutaro, A. (2021). Internal audit practice and financial reporting quality: Perspective from Nigerian quoted foods and beverages firms. KIU Interdisciplinary Journal of Humanities and Social Sciences, 2(1), 410-428. |

| [30] | Yemataw, S. D. (2022). Determinants of Internal Audit Effectiveness: The Case of Berhan Bank Sc and Abay Bank Sc (Doctoral Dissertation, Addis Ababa University). |

[22, 30]

has shown that perceived independence positively influences compliance with laws and regulations, as well as the quality of audit reports. These findings highlight the importance of independence in ensuring the integrity and effectiveness of internal audit processes, both in the private and public sectors.

In conclusion, the regression results and previous empirical evidence consistently demonstrate that independence is a significant factor in influencing the effectiveness of internal audit. IA independence positively contributes to the objective and unbiased assessment of controls and risks, enhancing the overall effectiveness of the internal audit function. Recognizing and promoting independence within the internal audit profession is vital for ensuring the integrity and value of internal audit activities.

4.3.3. Organizational Setting on the Effectiveness of Internal Audit

The third objective of this study aims to examine the effect of organizational setting on the effectiveness of internal audit.

Table 9 indicates the regression results of Organizational setting has an unstandardized coefficient is -0.331 with a standard error of 0.098. The t-value is -3.374, and the associated p-value is 0.001.

The coefficient for organizational setting indicates a positive relationship with internal audit effectiveness, specifically within the context of Lemikura subcity public sector. However, the p-value associated with this coefficient is 0.001, which is below the conventional significance level of 0.05. This implies that the relationship between organizational setting and internal audit effectiveness is statistically significant in the study. While the coefficient suggests a negative direction of the relationship with statistical significance indicates that when organizational setting increase in by one unit IA effectiveness decrease by 0.331 units keeping other things constant. In other words, the data does not provide strong evidence to conclude that organizational setting has a significant impact on internal audit effectiveness in this particular analysis.

The finding support by previous empirical evidences, for instance, studies conducted by

| [3] | Azzali, S., &Mazza, T. (2018). The internal audit effectiveness evaluated with an organizational, process and relationship perspective. International Journal of Business and Management, 13(6), 238-254. |

| [30] | Yemataw, S. D. (2022). Determinants of Internal Audit Effectiveness: The Case of Berhan Bank Sc and Abay Bank Sc (Doctoral Dissertation, Addis Ababa University). |

[3, 30]

argued that higher IA effectiveness in companies attributed to their greater flexibility and less bureaucratic nature. The studies found that public sector internal audit functions faced greater challenges in achieving effectiveness due to bureaucratic structures and political influences. In summary, the finding results show that the coefficient for "Organizational Setting" suggests a positive and a statistically significance relationship with internal audit effectiveness.

4.3.4. Audit Committee on the Effectiveness of Internal Audit

To show the impact of the presence of an audit committee on the effectiveness of internal audit is the fourth objective of the study. The coefficient is 0.362 with a standard error of 0.101. The standardized coefficient (Beta) is 0.276, indicating a statistically significant positive relationship with the Mean of IA Effectiveness (p = 0.000).

Table 9 shows the findings of an audit committee has a statistically significant positive impact on the effectiveness of internal audit. The coefficient suggests that for every one-unit increase in the audit committee, there is an estimated increase of 0.362 units in the IA Effectiveness. The standardized coefficient (Beta) of 0.276 further confirms this positive relationship (p = 0.000).

The findings align with previous research examining the impact of the audit committee on internal audit effectiveness.

| [5] | Brown, T., & Fanning, K. (2019). The joint effects of internal auditors' approach and persuasion tactics on managers' responses to internal audit advice. The Accounting Review, 94(4), 173-188. |

| [14] | Iyer, V. M., Jones III, A., &Raghunandan, K. (2018). Factors related to internal auditors' organizational-professional conflict. Accounting Horizons, 32(4), 133-146. |

[5, 14]

explored the impact of audit committee independence on internal audit effectiveness and found a significant positive relationship. Similarly,

| [19] | Mieseigha, E. G., &Adeyemi, A. A. (2021). Audit committee attributes and firm revenue growth in the Nigerian banking industry. Journal of Advanced Research in Management, 12(2), 47-53. |

| [29] | Yahaya, I. D., &Okoroigwe, E. S. (2022). Moderating Effect of Audit Committee Financial Expertise on the Relationship between Audit Quality and Earnings Management of Quoted Consumer Goods Firms in Nigeria. Lapai Journal of Economics, 6(2), 34-48. |

[19, 29]

emphasized the importance of an active and independent audit committee in family-controlled firms, as it enhances the effectiveness of the internal audit function through appropriate oversight and support. This aligns with the current study's results, suggesting that the presence of an audit committee, which is typically expected to be independent, positively influences Internal Audit Effectiveness.

In general, the findings of the current study are consistent with previous research, indicating that a strong, independent, and effective audit committee positively influences the effectiveness of internal audit. The support provided by the previous studies adds credibility to the current study's findings, reinforcing the importance of an active and supportive audit committee in enhancing IA Effectiveness.

4.3.5. Competency of Internal Auditor on the Effectiveness of Internal Audit

The fifth objective of the study was to examine the effect of competency of internal auditor on the effectiveness of internal audit. As shown in

table 9 the regression result of Internal Auditors Competency has the coefficient is 0.473 with a standard error of 0.130. The standardized coefficient (Beta) is 0.346, indicating a statistically significant positive relationship with the IA Effectiveness (p = 0.000).

The regression results indicate that the coefficient for the variable competency of internal auditor is indicating a positive relationship with internal audit effectiveness. The coefficient for the variable indicating that a 1 unit increase in the competency of internal auditors leads to a 0.473 unit increase in internal audit effectiveness is based on the findings of the study. This coefficient is statistically significant (p-value: <0.05), suggesting that the competency of internal auditors has a significant impact on internal audit effectiveness.

A study supports the notion that the presence of adequate and competent internal audit staff is positively related to internal audit effectiveness

| [30] | Yemataw, S. D. (2022). Determinants of Internal Audit Effectiveness: The Case of Berhan Bank Sc and Abay Bank Sc (Doctoral Dissertation, Addis Ababa University). |

[30]

. Competent internal auditors possess the necessary skills and expertise to contribute significantly to the effectiveness of internal audit. Similarly,

| [9] | George, D., Theofanis, K., &Konstantinos, A. (2015). Factors associated with internal audit effectiveness: Evidence from Greece. Journal of Accounting and Taxation, 7(7), 113-122. |

| [17] | Kassie, W. D. (2021). Bank Specific Determinants of Internal Audit Effectiveness: Evidence from Private Banks in Ethiopia. European Journal of Business and Management, 13(5), https://doi.org/10.7176/EJBM/13-5-0 |

[9, 17]

also found evidence supporting a positive relationship between the competency of internal auditors and internal audit effectiveness.

Overall, the empirical evidence from the reviewed studies consistently supports this study finding that the competency of internal auditors plays a crucial role in determining the effectiveness of internal audit. When internal auditors possess the necessary knowledge, skills, and abilities, they are better equipped to perform their duties effectively, resulting in improved internal audit outcomes. Investing in the training, development, and recruitment of competent internal auditors becomes essential to enhance the effectiveness of internal audit processes within organizations. By ensuring that internal auditors have the necessary competencies and staying up-to-date with emerging trends and best practices, organizations can strengthen their internal audit function and its ability to provide valuable insights and assurance.

Generally, the regression results indicate a statistically significant and positive relationship between the competency of internal auditors and internal audit effectiveness. The reviewed empirical studies consistently support this relationship, highlighting the importance of competent internal auditors in improving the effectiveness of internal audit. The organizations should prioritize investments in developing and maintaining the competencies of their internal auditors to enhance the overall effectiveness of their internal audit function.